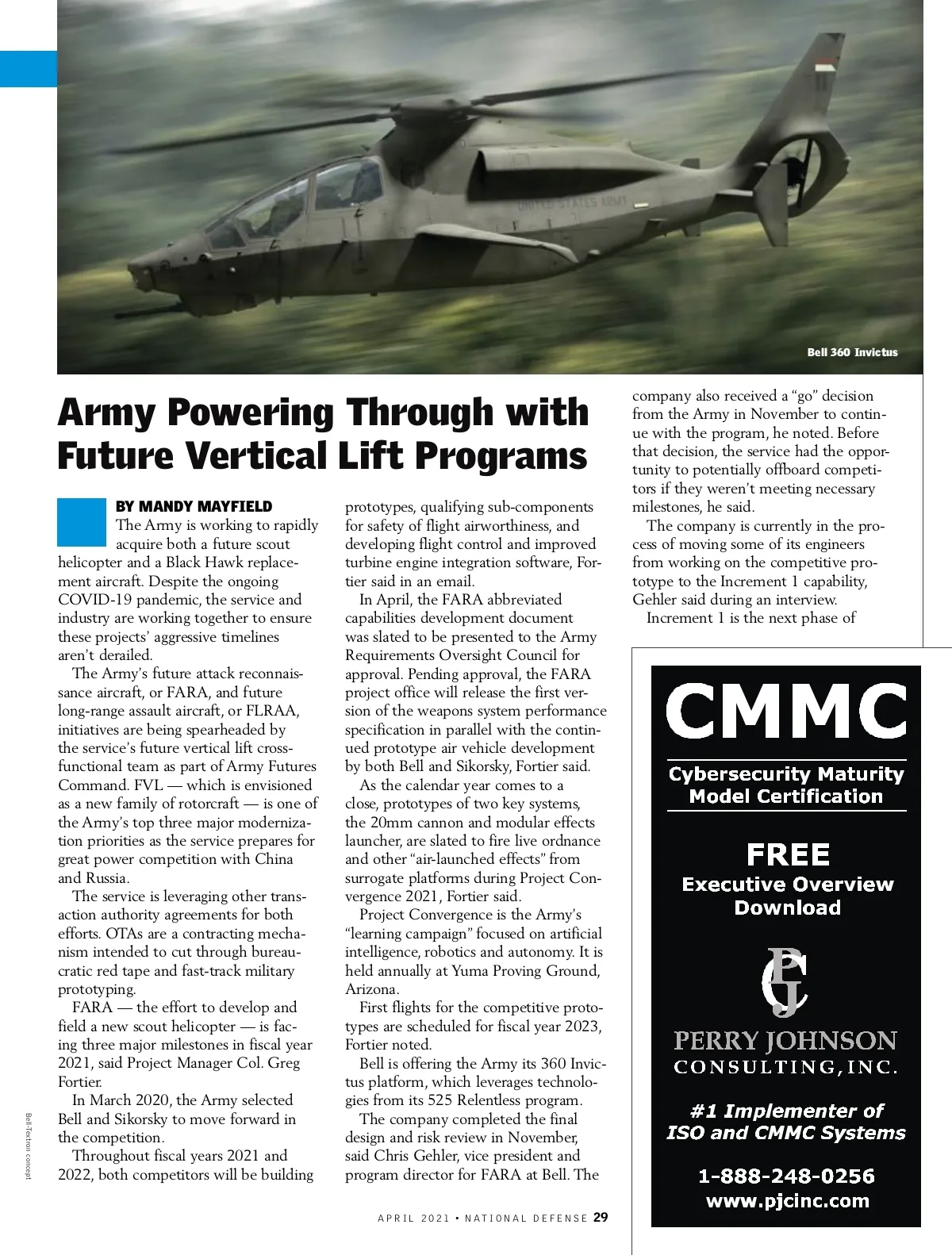

ROTARY WING able to find alternatives.” Instead of seeing direct delays, the challenge the office is seeing so far is general inefficiency, Barrie noted. How-ever, that’s a difficult thing to quantify, he added. “We would all acknowledge that things aren’t as efficient as they perhaps were before COVID,” he said. “Yet if I asked you to quantify it for me and tell me exactly how efficient we’re being, that’s a very challenging thing to do. …We don’t have a direct correlation. There’s not a, ‘Hey, we are X percent less efficient.’” The Army has been working to sup-port industry by opening communica-tion lines with companies to ensure acquisition strategies and procurement plans are clearly understood to help with resourcing, Barrie said. The service is also working to obligate funds quickly to companies for ongoing work, he said. “We’ve [been] working with our contracting partners, making sure that when a contractor bills us for work that they’ve done, that we are rap-idly dispersing those dollars out to our contractors to make sure that if they do have ... an invoice into the government for a revenue that we’re able to pay that in a timely fashion,” he said. That’s a practice the program office has always endeavored to do, but with companies jug-gling debt from COVID-related expenses it is doubling down, Barrie added. Jaworowski in the short term said he expected production in the military rotorcraft market to gain ground “fairly strongly” in 2021 and 2022 as supply issues are resolved. By 2022, he expects the num-ber of platforms built to be on par with what was produced in 2019. However, there are longer-term issues that may stifle growth as the decade continues, he noted. That includes declining or flat military budgets, which will be a top concern for industry. “In real terms, fiscal ’21 was down a little bit and we don’t know what the next budget request is going to look like,” he said. “It does seem that some cuts may yet be coming, so it looks like 28 NATIONAL DEFENSE • APRIL 2021 the peak was probably fiscal ’20.” Meanwhile, as the 2020s continue, the military rotorcraft market will see legacy programs — such as the UH-60 Black Hawk, AH-64 Apache and the V-22 Osprey — start to wind down, he said. “The services are well on their way to completing those programs and by 2030, many of those will have ended or be very close to being ended,” he said. “Now that’s not to say production of those models will cease at that point — you will have production for export, of course — but because U.S. procurement will be at, or near the end, the annual build rates will be lower than when the U.S. programs of record were really in full swing.” Jaworowski noted that the CH-47F Block II Chinook program may be an outlier. “There seems to be considerable sup-port in Congress to reviving that pro-gram. … We do expect it to be revived at some point,” he said. The fiscal year 2022 presidential budget request will likely provide more clarity, he added. After 2022, production in the military rotorcraft market will gradually decline for a time, Jaworowski predicted. Like the United States, many countries’ replacement cycles for their helicopter acy designs that had been in their fleet for years and years and years — a new version of Black Hawk, a new version of Apache, a new version of Chinook, a new version of the Huey.” The V-22 Osprey tiltrotor aircraft is the only all-new rotorcraft that the United States has procured in decades, he noted. The service tried to build an armed reconnaissance aircraft known as the RAH-66 Comanche but that project was canceled before it went into pro-duction. “There was a concern for a while there of a lack of innovation in the U.S. industrial base,” he said. The Army National Guard’s UH-72A Lakota was based on the Eurocopter EC145, which is now part of the Airbus Group Inc. The service has procured 400 of the European-designed aircraft over the past decade. “European manufacturers kind of stole the march a little bit back then in terms of product innovation, because they put out new models whereas the U.S. manufacturers were quite understand-ably simply responding to what the Pen-tagon was asking for, which was simply a newer version of what was already in their fleet,” Jaworowski said. Future vertical lift has injected much needed product innovation into the industry, he said. While the pandemic has caused a few months delay to the initia-tive, it is unlikely to cause any seri-ous issues, said Rhys McCormick, a fellow at the Center for Strategic and International Studies’ Defense-Industrial Initiatives Group and co-author of the center’s report on the helicopter industry. AH-64 Apache However, a longer delay could spell trouble. fleets are coming to an end, although “A few months delay will not end the there will still be some export opportu-industrial base, but if they’re starting nities in regions such as the Asia-Pacific to talk about pushing programs back a and the Middle East, he added. year or two years, that’s when you start However, efforts such as future verti-running into some of the more serious cal lift in the late 2020s and early 2030s issues about how the transition is going will be a big boost to the market, he to happen between the legacy programs noted. and the next-gen programs,” he said. It’s “hard to overstate the long-term Right now, the Army is in a pre-importance of future vertical lift to the decisional stage when it comes to future military rotorcraft industry,” Jaworowski vertical lift, he said. But as it grows clos-said. “For decades the U.S. military was er to reaching a decision, that’s when simply buying the latest version of leg-delays become more significant. ND Army photo

National Defense Digital April 2021: Page-28